Getting approved for a mortgage in Virginia — whether you’re buying in Richmond, Chesterfield, Fredericksburg, or Virginia Beach — comes down to a handful of measurable factors: credit profile, debt-to-income ratio, documentation quality, and lender access. The encouraging reality is that each of these factors is addressable before you ever submit a formal application.

This list covers nine tools that Virginia homebuyers and mortgage seekers in Florida, Tennessee, and Georgia can use right now to strengthen their approval position. Each tool is evaluated on what it actually does, who it’s built for, and where it fits in the approval process. No tool here is a guarantee — mortgage approval depends on your full financial picture — but each one gives you a measurable edge.

Tools are ordered by impact on the approval process, with the broadest-reach tool first.

Loan Type Quick Reference: Virginia, FL, TN, and GA

Before diving into the tools, here is the baseline data every borrower should know. Your loan type determines the credit score floor, down payment requirement, and DTI ceiling that the tools below are helping you meet.

Loan Type | Min Credit Score | Min Down Payment | DTI Max | Notes

FHA | 580 (500 w/ 10% down) | 3.5% | ~57% | Available VA, FL, TN, GA

Conventional | 620 | 3% | ~45% | PMI required below 20% down

VA Loan | 580 (lender overlay) | 0% | ~41% (flexible) | Veterans and active military

USDA | 640 | 0% | ~41% | Rural Virginia areas eligible

Bank Statement | 620+ (varies) | 10–20% | Varies | Self-employed borrowers

DSCR | 620+ | 20–25% | N/A (rental income used) | Investment properties

Source: HUD.gov, VA.gov, USDA Rural Development. Program guidelines are subject to change. Not all borrowers will qualify.

Why Credit Score Improvement Has Real Dollar Value

Here is a worked example showing why the tools in this list matter in concrete financial terms. This is illustrative math using standard amortization — not a rate quote or guarantee.

Scenario: $350,000 purchase price, 10% down, $315,000 loan amount, 30-year fixed.

At 7.25% (credit score 620): Monthly principal and interest = approximately $2,150

At 6.875% (credit score 680): Monthly principal and interest = approximately $2,069

Monthly savings: approximately $81

Annual savings: approximately $972

10-year savings: approximately $9,720

A 60-point credit score improvement — achievable with several of the tools below — can translate to nearly $10,000 in payment savings over a decade on a mid-range Virginia purchase. That is the math behind why preparation before application matters.

1. Free Mortgage Search

Best for: Virginia, FL, TN, and GA borrowers who want to compare hundreds of lenders without a credit hit

Free Mortgage Search is a multi-lender mortgage search and comparison platform that shops hundreds of lenders simultaneously using Vantage Score 4.0, a soft-pull model that does not affect your credit score.

Where This Tool Shines

Most single-lender institutions — banks, credit unions, and many of the large retail lenders like Rocket Mortgage, Movement Mortgage, or PrimeLending — run a hard credit pull before showing you rates. That inquiry appears on your credit report and can reduce your score by several points, remaining visible for 24 months. Free Mortgage Search uses Vantage Score 4.0, which is a soft pull. You see real rate comparisons across hundreds of lenders with zero credit score impact.

This matters most for borrowers who are near an approval threshold. If your score is 618 and you need 620 for a conventional loan, multiple hard inquiries from rate shopping could push you further from the target. The NoTouch Credit approach eliminates that risk entirely while giving you broader market access than any single lender can provide.

Key Features

NoTouch Credit (Vantage Score 4.0): Soft-pull credit model with zero hard inquiry impact — your score is not affected by the search process.

Hundreds of Lenders Compared Simultaneously: Single-lender institutions show you one rate. This platform shows you the competitive landscape across a wide network in one session.

Credit Scores Accepted Down to 500: Many competitors set floors at 620 or 640. Free Mortgage Search accesses lenders who work across the full credit spectrum, including FHA-eligible borrowers at 500 with 10% down.

Cash-Out Refinance to 90% LTV: Many lenders cap cash-out refinances at 80–85% LTV. The 90% LTV access through this network gives homeowners in Richmond, Chesterfield, and Hampton Roads more equity flexibility.

Bank and Credit Union Turndown Conversions: Self-employed borrowers in Richmond turned down due to tax return income documentation, or buyers in Chesterfield declined for a 545 credit score at a credit union with a 620 floor, frequently find alternative program paths through the lender network here.

Best For

Any homebuyer or refinance borrower in Virginia, Florida, Tennessee, or Georgia who wants to compare the market without credit score exposure. Especially valuable for borrowers with credit scores below 620, self-employed borrowers, and anyone who has received a bank or credit union turndown.

Pricing

Free to search and compare. There is no cost to the borrower for the search and comparison process.

How Free Mortgage Search Compares to Local Competitors

Local Richmond-area lenders like Sparrow Home Loans, 804 Mortgage, C&F Mortgage (Valerie Holbrook), and Parks Mortgage Group serve Virginia borrowers well and provide relationship-based service. The distinction with Free Mortgage Search is structural: those are individual lenders or loan officers presenting their own product set. Free Mortgage Search is a search platform that presents hundreds of lenders’ products simultaneously, with no hard credit pull to initiate the comparison.

For borrowers who already know which lender they want to work with, those local relationships have real value. For borrowers who want to see the full market before committing — or who have been turned down elsewhere — the platform model provides access that a single-lender relationship cannot replicate.

Speed to close is also a documented differentiator in competitive Virginia markets. In Fredericksburg, Spotsylvania, and Short Pump, where sellers routinely receive multiple offers, a 21-day close capability versus a 45-day retail bank timeline can be the difference between winning and losing a contract.

2. AnnualCreditReport.com

Best for: Every borrower — the mandatory first step before any mortgage application

AnnualCreditReport.com is the only federally authorized source for free credit reports from all three major bureaus: Equifax, Experian, and TransUnion.

Where This Tool Shines

This is not a credit monitoring app or a score estimator. This is the actual report — the same data that lenders pull when they evaluate your application. Errors on credit reports are more common than most borrowers expect. A collection account that was paid but not updated, a balance reported higher than the actual amount, or an account that belongs to someone else with a similar name can all suppress your score without your knowledge.

Identifying and disputing these errors before a lender sees them is one of the highest-leverage moves a borrower can make. The dispute process under the Fair Credit Reporting Act requires bureaus to investigate and correct verified errors, typically within 30 days. Finding an error six months before you apply gives you time to resolve it cleanly.

Key Features

Reports from All Three Bureaus: Equifax, Experian, and TransUnion each maintain separate files. Errors on one bureau do not automatically appear on others — you need all three.

Weekly Access Available: The weekly free report policy, maintained after its COVID-era expansion, means you can monitor your file throughout the credit improvement process.

Federally Authorized, No Subscription Required: No credit card, no upsell, no enrollment. This is a statutory right under the FCRA.

Starting Point for Dispute Process: Every formal dispute begins with the information in this report. You cannot dispute what you have not reviewed.

Identifies Derogatory Marks Before Lenders See Them: Collections, late payments, charge-offs, and public records are all visible here — and each one is addressable before application.

Best For

Every borrower, without exception. Pull all three reports at least 90 days before you plan to apply. If you find errors, that buffer gives you time to file disputes and have corrections reflected before a lender runs their own inquiry.

Pricing

Free under federal law. No subscription or payment method required at AnnualCreditReport.com.

3. Credit Karma

Best for: Ongoing credit monitoring, score trend tracking, and payoff scenario modeling

Credit Karma provides free credit monitoring using TransUnion and Equifax VantageScore data, with alerts for new accounts, hard inquiries, and balance changes.

Where This Tool Shines

Credit Karma’s score simulator is particularly useful in the pre-application phase. You can model scenarios — what happens to your score if you pay off a specific card, or if you open a new account — before taking action. This helps borrowers prioritize which debts to address first for maximum score impact.

One important distinction: Credit Karma displays VantageScore, not FICO. Most mortgage lenders use FICO Score models (typically FICO 2, 4, or 5 for mortgage decisions). Your Credit Karma score and your mortgage FICO score will likely differ. Use Credit Karma as a directional indicator and trend tracker, not as the definitive number your lender will see.

Key Features

Score Simulator: Models the projected impact of paying off balances, closing accounts, or opening new credit before you take action.

Real-Time Alerts: Notifies you of new accounts, hard inquiries, and significant balance changes — useful for catching identity theft early.

Free Monitoring on Two Bureaus: TransUnion and Equifax data updated regularly, with no cost and no hard inquiry.

Spending Tracker: Basic budgeting features help identify where cash flow can be redirected toward debt paydown.

Best For

Borrowers actively working to improve their credit score in the 6–12 months before a mortgage application. Use it alongside AnnualCreditReport.com — one gives you the full report, the other gives you ongoing monitoring and modeling tools.

Pricing

Free. Credit Karma generates revenue through financial product recommendations, not user fees.

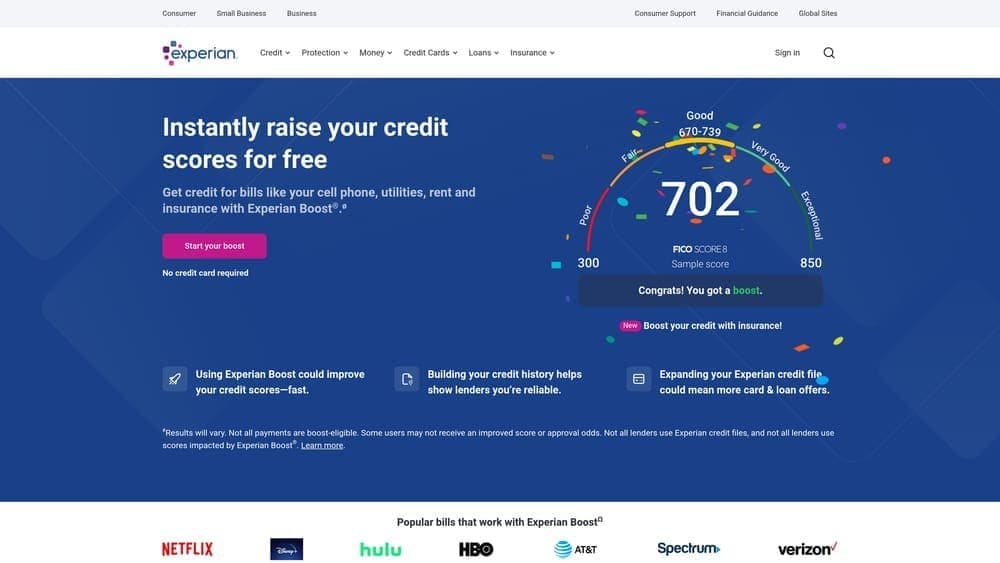

4. Experian Boost

Best for: Borrowers with thin credit files or scores just below a key threshold

Experian Boost adds utility payments, phone bills, and eligible streaming service payment history to your Experian credit file, potentially increasing your Experian-based credit scores.

Where This Tool Shines

Traditional credit scoring ignores on-time utility and phone payments entirely. Experian Boost captures that payment history and incorporates it into your Experian file. For borrowers with limited credit history — recent graduates, borrowers who have avoided credit cards, or anyone with a thin file — this can add meaningful positive payment history without opening new accounts.

Score impact varies by individual and is not guaranteed. Borrowers with already-robust credit histories may see minimal change. Borrowers with thin files or those who have been consistent with utility payments for several years tend to see the most benefit.

Key Features

No Hard Inquiry: The Boost process does not trigger a hard credit pull and does not affect your score negatively.

Adds Utility, Phone, and Streaming History: Captures payment data that traditional scoring models ignore entirely.

Instant Impact: Score changes, when they occur, are reflected immediately after the connection is made.

Free to Use: No cost to the borrower for the Boost feature.

Experian FICO Score Access: Experian provides your FICO Score 8 alongside the Boost tool, giving you a closer approximation of what lenders may see than VantageScore-based tools.

Best For

Borrowers with credit scores in the 560–620 range who have consistent utility and phone payment history. If you are a few points below a conventional loan threshold, this is a low-risk tool worth running before any other credit action.

Pricing

Free. Experian offers paid subscription tiers for additional monitoring features, but Boost itself carries no cost.

5. CFPB Owning a Home Toolkit

Best for: First-time buyers who need a lender-neutral framework for evaluating mortgage offers

The CFPB Owning a Home resource provides government-issued, lender-neutral guidance on shopping for mortgage rates, understanding Loan Estimates, and comparing APR across lenders.

Where This Tool Shines

Most mortgage marketing is produced by lenders. The CFPB resource is produced by the federal agency that regulates them. That distinction matters when you are trying to understand what a Loan Estimate actually means, how to compare APR versus interest rate, or what fees are negotiable versus fixed.

The “Your Home Loan Toolkit” is a HUD/CFPB-required document for purchase loans — lenders are required to provide it. Reading it before you receive it from a lender puts you in a much stronger negotiating position when comparing offers from multiple sources.

Key Features

Rate Shopping Guide: Explains how to compare Loan Estimates across lenders on an apples-to-apples basis.

Loan Estimate Walkthrough: Line-by-line explanation of the standardized Loan Estimate form all lenders must provide.

APR vs. Interest Rate Explanation: Clarifies why APR is the more complete comparison metric.

Closing Cost Breakdown: Identifies which fees are lender-controlled versus third-party, and which are negotiable.

Best For

First-time buyers in Richmond, Charlottesville, Williamsburg, or any Virginia market who are receiving their first Loan Estimates and want an unbiased framework for comparison. Also useful for any borrower who has not purchased in several years and wants to understand how the current disclosure process works.

Pricing

Free. Government-issued resource with no registration required.

6. Zillow Mortgage Calculator

Best for: DTI modeling and full payment estimation before application

Zillow’s mortgage calculator includes principal, interest, property taxes, homeowners insurance, and HOA fees in its payment estimate, making it one of the more complete pre-application modeling tools available.

Where This Tool Shines

Debt-to-income ratio is one of the four primary variables in mortgage approval, and it is the one borrowers most frequently underestimate. Lenders calculate DTI using your total monthly debt obligations divided by your gross monthly income. A PITI payment (principal, interest, taxes, insurance) that looks affordable based on the loan amount alone can push DTI over the lender’s threshold when property taxes and insurance are added.

Virginia property tax rates vary significantly by locality. Henrico County, Chesterfield, and Virginia Beach each carry different effective tax rates. Running your target purchase price through a calculator that includes local tax estimates gives you a more accurate DTI picture than a simple principal-and-interest calculation.

Key Features

Full PITI Calculation: Includes principal, interest, taxes, insurance, and HOA — the same components lenders use for DTI calculation.

Adjustable Inputs: Modify rate, down payment, loan term, and property tax rate to model different scenarios.

DTI Pre-Check: Divide the estimated monthly payment by your gross monthly income to see where you stand before a lender does the same math.

Amortization Schedule: Shows the principal vs. interest breakdown over the loan term, useful for evaluating 15-year versus 30-year options.

Best For

Any borrower in the early planning phase who wants to establish a realistic purchase price ceiling based on their income and existing debt obligations. Run this calculation before you begin home shopping, not after you find the house you want.

Pricing

Free. No account required to use the calculator.

7. YNAB (You Need A Budget)

Best for: Borrowers building down payment savings or reducing DTI through disciplined cash flow management

YNAB is a zero-based budgeting platform that assigns every dollar of income to a specific category, making it particularly effective for borrowers who need to accelerate savings or reduce debt balances before applying.

Where This Tool Shines

DTI reduction requires either increasing income or decreasing debt. For most borrowers, decreasing debt is the more immediately controllable variable. YNAB’s structure forces you to make explicit decisions about where every dollar goes, which tends to surface discretionary spending that can be redirected toward debt paydown or down payment savings.

For buyers in competitive Virginia markets like Short Pump, Glen Allen, or Midlothian, where median home prices require meaningful down payments, the discipline of tracking savings progress in real time against a specific target date keeps the process concrete rather than aspirational.

Key Features

Zero-Based Budgeting Framework: Every dollar of income is assigned a purpose, eliminating passive spending that erodes savings capacity.

Debt Paydown Tracking: Visualizes progress toward eliminating specific balances, which directly improves DTI.

Goal Tracking: Set a down payment target with a deadline and track monthly progress against it.

Bank Sync: Connects to most major financial institutions for automatic transaction import.

Best For

Borrowers who are 6–18 months from a purchase and need to build down payment savings, pay down revolving debt to improve credit utilization, or reduce monthly debt obligations to meet a DTI threshold.

Pricing

YNAB charges a subscription fee. Check ynab.com for current pricing. A free trial is available.

8. IRS Get Transcript

Best for: Borrowers who want to accelerate underwriting by having income documentation ready before it is requested

IRS Get Transcript provides direct access to your tax return transcripts — the same documents lenders request via IRS Form 4506-C during the underwriting process.

Where This Tool Shines

Underwriting delays are frequently caused by the 4506-C income verification process. Lenders submit the form to the IRS, and the IRS response time adds days or weeks to the timeline. In competitive Virginia markets where a 21-day close is the difference between winning and losing a contract, any tool that compresses underwriting time has direct financial value.

Having your tax transcripts already in hand when you begin the application process allows your loan officer to verify income documentation upfront rather than waiting for the IRS response mid-underwriting. This is particularly relevant for self-employed borrowers in Richmond, Goochland, or Charlottesville whose income documentation is more complex than a standard W-2.

Key Features

Direct IRS Access: Pull your own transcripts immediately rather than waiting for lender-initiated requests.

Tax Return Transcript: Shows the data from your filed return — the primary document lenders use for income verification.

Wage and Income Transcript: Shows W-2, 1099, and other income forms reported to the IRS — useful for verifying all income sources.

Account Transcript: Shows tax account status, which lenders may review to confirm no outstanding tax liabilities.

Best For

Self-employed borrowers, W-2 employees with multiple income sources, and any borrower in a time-sensitive purchase situation where underwriting speed is a priority. Pull your last two years of transcripts before your first lender conversation.

Pricing

Free through the IRS website. No cost to access your own transcripts.

9. HUD Housing Counselor Locator

Best for: Borrowers who want lender-neutral, one-on-one guidance from a HUD-approved counselor

HUD’s Housing Counselor Locator connects borrowers with HUD-approved housing counselors who provide lender-neutral pre-purchase guidance across Virginia and the other states served by Free Mortgage Search.

Where This Tool Shines

Every other tool on this list gives you data or modeling capability. A HUD-approved counselor gives you a human conversation with someone who has no financial interest in which lender you choose. They can review your full financial picture, help you understand your loan options, and identify steps you should take before applying — without steering you toward any particular product.

HUD counselors are available across Virginia, including in Hampton Roads, Roanoke, Lynchburg, and the Fredericksburg corridor. For borrowers who have been turned down before, are navigating a complex income situation, or simply want an independent second opinion before committing to a lender, this resource fills a gap that no app or calculator can.

Key Features

Lender-Neutral Guidance: HUD-approved counselors are not affiliated with lenders and do not earn commissions on loan placement.

Pre-Purchase Counseling: Covers credit, budgeting, loan types, and the purchase process in a personalized session.

Statewide Availability: Counselors serve Virginia cities including Richmond, Virginia Beach, Norfolk, Roanoke, Lynchburg, Charlottesville, and Fredericksburg.

Low or No Cost: Many HUD-approved counseling sessions are available at low or no cost to the borrower.

Best For

First-time buyers, borrowers with complex financial situations, and anyone who has received a mortgage denial and wants an independent assessment of their options before applying again.

Pricing

Varies by agency. Many HUD-approved counselors provide services free of charge or on a sliding scale. Confirm directly with the agency you select through the locator.

Frequently Asked Questions

Does shopping multiple lenders hurt my credit score?

It depends on how you shop. Traditional lender inquiries are hard pulls that appear on your credit report and can reduce your score. However, FICO scoring models typically treat multiple mortgage inquiries within a 14–45 day window as a single inquiry for rate-shopping purposes. Free Mortgage Search uses Vantage Score 4.0, a soft-pull model, which means the initial comparison process does not generate a hard inquiry at all and does not affect your score.

What credit score do I need to get approved for a mortgage in Virginia?

It depends on the loan type. FHA loans are available with scores as low as 580 with 3.5% down, and some lenders will go to 500 with 10% down. Conventional loans typically require 620 or higher. VA loans for eligible veterans have no official minimum but most lenders apply overlays of 580–620. USDA loans for rural Virginia areas typically require 640. Free Mortgage Search accesses lenders across this full spectrum, including lenders who work with scores as low as 500.

What is a NoTouch Credit check?

A NoTouch Credit check uses Vantage Score 4.0, a soft-pull credit model, to assess your credit profile without generating a hard inquiry. Unlike a traditional hard pull, this process does not appear on your credit report and does not reduce your credit score. It allows borrowers to receive real rate comparisons from multiple lenders without the credit score exposure that typically comes with rate shopping.

Can I get approved for a mortgage after being turned down by a bank?

Yes, in many cases. Banks and credit unions operate under their own internal underwriting guidelines, which are often more restrictive than the full range of available loan programs. Common turndown scenarios include self-employed borrowers whose tax returns show reduced net income after business deductions, borrowers with credit scores below a bank’s internal floor, and borrowers whose DTI exceeds a specific institution’s threshold. Alternative lenders — including bank statement loan programs for self-employed borrowers and FHA lenders with lower score floors — can often provide a path to approval where a traditional bank cannot. The Free Mortgage Search network includes lenders who specialize in these scenarios.

How long does it take to improve my credit score before applying?

Timeline varies based on what is suppressing your score. Paying down revolving credit card balances can show improvement within one to two billing cycles. Disputing and correcting errors through the FCRA process typically takes 30–45 days per dispute. Negative items like late payments or collections have a diminishing impact over time but do not disappear immediately. For most borrowers targeting a meaningful score improvement, a 3–6 month runway before application provides adequate time for most credit actions to be reflected.

What is the difference between VantageScore and FICO?

VantageScore and FICO are two different credit scoring models developed by different companies. FICO scores are used by the majority of mortgage lenders — specifically FICO 2 (Experian), FICO 4 (TransUnion), and FICO 5 (Equifax) for mortgage decisions. VantageScore, developed jointly by the three bureaus, is used by many consumer-facing credit monitoring tools including Credit Karma and is the basis for the Vantage Score 4.0 soft-pull model used by Free Mortgage Search. The two models can produce different scores for the same borrower. Treat VantageScore-based tools as directional indicators, not as the definitive number your mortgage lender will use.

What DTI ratio do lenders want to see?

Most conventional lenders prefer a total back-end DTI (all monthly debt payments divided by gross monthly income) at or below 43–45%. FHA loans allow DTI up to approximately 57% with compensating factors. VA loans are flexible but most lenders prefer DTI at or below 41%. USDA loans generally follow similar guidelines. DTI is calculated using your proposed housing payment (PITI) plus all existing monthly debt obligations. Reducing credit card balances, paying off installment loans, or increasing income before application are the primary levers for improving DTI.

Which Tool Is Right for Your Situation

The nine tools above cover the full approval preparation spectrum, but not every borrower needs all nine. Here is a quick-reference guide by situation.

Starting from scratch, no idea where you stand: Begin with AnnualCreditReport.com to pull all three bureau reports, then run a comparison through Free Mortgage Search to see what lenders and programs are available to you right now.

Credit score below 620, previously turned down by a bank or credit union: Free Mortgage Search is your primary tool. The network accesses lenders who work with scores as low as 500 and includes bank statement loan programs for self-employed borrowers. The NoTouch Credit process means you can explore your options without further credit score exposure.

Score near a threshold (615–635) and trying to optimize before applying: Combine AnnualCreditReport.com (dispute any errors), Experian Boost (add utility payment history), and Credit Karma (model payoff scenarios) before running a formal comparison.

Self-employed borrower with strong deposits but complex tax returns: IRS Get Transcript gives you your income documentation in advance. Free Mortgage Search connects you with bank statement loan lenders who qualify on deposits rather than tax return net income.

Competitive market, time-sensitive close (Richmond, Short Pump, Fredericksburg): Free Mortgage Search’s speed-to-close advantage in the lender network is directly relevant here. Having IRS transcripts ready and documentation organized before application compresses underwriting time further.

First-time buyer who wants to understand the process before talking to any lender: Start with the CFPB Owning a Home Toolkit and a HUD Housing Counselor session. Both are lender-neutral and give you the framework to evaluate any offer you receive.

Mortgage approval is a preparation problem as much as a qualification problem. The borrowers who get the best outcomes are typically the ones who addressed their credit, documentation, and lender access before the formal application — not during it.

Start your free mortgage search today to compare rates from hundreds of lenders simultaneously, with no credit score impact and no cost to search.